Hong Kong Mortgage Guide 2026: H-Rate, P-Rate, Fixed Rate and Mortgage Insurance

Buying a home in Hong Kong is often seen as a major financial milestone. For many buyers, the property market may feel expensive and complicated, but the truth is that getting onto the property ladder is not as difficult as it seems if you understand the basics of mortgage lending, affordability, and loan structure.

In Hong Kong, residential property is often viewed as a relatively resilient asset, which is why it is commonly called “brick.” It remains popular among both owner-occupiers and global investors. But before making a purchase, one of the most important steps is understanding how a mortgage works. From mortgage types and loan-to-value ratios to mortgage insurance and refinance options, knowing the rules can help you make a more confident decision.

This guide explains the essentials of Hong Kong mortgages in simple English, so first-time buyers and experienced homeowners alike can better understand the process.

What Is a Mortgage?

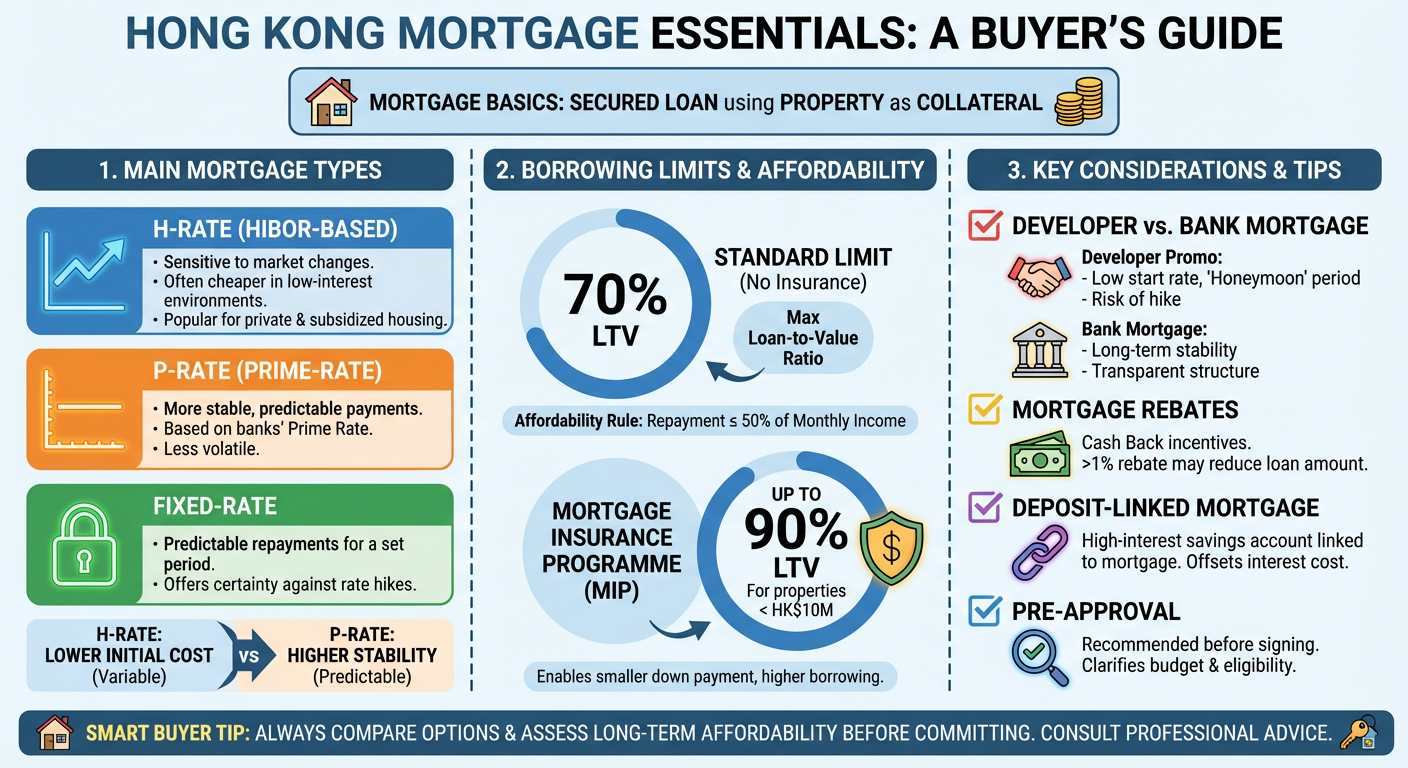

A mortgage is a secured loan that uses a property as collateral. In simple terms, when you buy a home but do not want to pay the full amount upfront, you borrow money from a bank or finance company and repay it over time with interest.

The repayment period, interest rate, and loan amount all affect how much you pay each month. That is why mortgage planning is such an important part of the home-buying process.

| Mortgage Type | Interest Rate |

|---|---|

| New Purchase | H+1.3%, Cap P-1.75%(Interest rate: 3.25%) |

| Refinance | H+1.3%, Cap P-1.75%(Interest rate: 3.25%) |

| HOS | H+1.3%, Cap P-1.75%(Interest rate: 3.25%) |

| Industrial Building/Commercial Building | P-0.5% |

| Car Park | P-0.5% |

When Should You Apply for a Mortgage?

In most cases, buyers apply for a mortgage after signing the provisional sale and purchase agreement. However, some banks also offer pre-approval services. This allows buyers to check whether they are likely to qualify for financing before signing the contract. Pre-approval can be especially helpful because it gives you a clearer idea of your budget and reduces the risk of choosing a property that may be difficult to finance.

Main Types of Hong Kong Mortgages

Hong Kong mortgage products generally fall into three main categories: H-rate mortgage, P-rate mortgage, and fixed-rate mortgage. Each one has its own advantages depending on market conditions and your repayment preference.

HIBOR-based Mortgage

A HIBOR-based Mortgage is based on HIBOR, or the Hong Kong Interbank Offered Rate. This is one of the most popular mortgage choices in Hong Kong. The main appeal of H-rate mortgages is that they can be more cost-effective in a low-interest environment. They are commonly available for private flats, village houses, old tenements and subsidized housing properties.

P-rate Mortgage

A P-rate mortgage, or P-Plan, is based on the Prime Rate set by banks. The Prime Rate tends to change less often than HIBOR, which makes this option more stable from a repayment perspective.Because of that stability, monthly instalments may be easier to predict. However, when market rates are low, H-rate mortgages are often cheaper overall.

Fixed-rate Mortgage

A fixed-rate mortgage offers predictable repayments for a set period. In Hong Kong, fixed-rate options may be provided by the Hong Kong Mortgage Corporation or by major banks through short-term fixed-rate plans.

These plans are usually attractive to buyers who prefer certainty and want to avoid short-term interest-rate fluctuations.

Mortgage Loan Limits in Hong Kong

The maximum mortgage ratio depends on the property type and whether mortgage insurance is used. Without mortgage insurance, the standard maximum loan-to-value ratio is generally 70 percent.

For insured mortgages, the borrowing limit can be higher, especially for properties under HK$10 million. In some cases, insured mortgages may allow up to 90 percent financing, subject to the property value band and the borrower’s eligibility.

As a general affordability rule, monthly mortgage repayment should not exceed 50% of monthly income.

Mortgage Insurance Programme

Mortgage Insurance Programme helps buyers borrow more than the standard loan-to-value limit. This is especially useful for buyers who want to purchase a home with a smaller down payment.The insured mortgage structure depends on the property price. Lower-value properties can usually enjoy higher financing ratios, while more expensive properties face tighter caps. This makes mortgage insurance a useful option for first-time buyers, but it is important to understand the loan bands and requirements before applying.

Developer Mortgage vs Bank Mortgage

New developments often come with promotional mortgage packages arranged by developers and finance companies. These may look attractive because they can offer lower interest rates at the beginning and may not require a stress test.

However, these plans often come with a honeymoon period of about two to three years. After that, the interest rate may rise significantly, which means the buyer may need to refinance later to reduce costs.Bank mortgages are usually more stable in the long run, especially for buyers who want a more traditional and transparent repayment structure.

How Mortgage Rebates Work

Banks may offer cash rebates to attract borrowers. These rebates can reduce your effective cost, but they do not always work the way buyers expect.

If the rebate is below 1 percent, it usually does not affect the loan amount calculation. If it is above 1 percent, part of the rebate may need to be deducted from the approved loan amount, which can increase the buyer’s upfront cash requirement.

That is why it is important to check the actual net benefit rather than focusing only on the advertised rebate amount.

What Is a Deposit-Linked Mortgage?

A Deposit-Linked Mortgage provides a high-interest savings account linked to your mortgage. It allows you to place spare funds into the account and earn interest that is usually tied to your mortgage rate.

This can be useful if you have extra savings and want to reduce your interest expense while still keeping your money accessible. Because it is a demand deposit account, you can withdraw the funds whenever necessary.

Mortgage Tips for First-time Buyers

First-time buyers in Hong Kong should pay close attention to a few key factors before applying for a mortgage.

• Check your affordability based on monthly income and future repayment pressure.

• Understand the difference between H-rate, P-rate, and fixed-rate mortgages.

• Review whether mortgage insurance is needed.

• Compare the benefits of bank mortgages and developer mortgage plans.

• Watch out for valuation risk, especially in the second-hand market.

• Consider the impact of age and property age on repayment period.

These factors can significantly affect the final loan amount, interest cost, and approval outcome.

FAQ

What are the main mortgage types in Hong Kong?

The main mortgage types in Hong Kong are H-rate mortgage, P-rate mortgage, and fixed-rate mortgage.

How much can I borrow for a Hong Kong property?

Without mortgage insurance, the standard maximum loan ratio is usually 70 percent. With mortgage insurance, borrowing can go up to 90 percent for properties under HK$10 million, subject to eligibility.

What is the H-rate mortgage?

An H-rate mortgage is based on HIBOR, which is the Hong Kong Interbank Offered Rate. It is one of the most common mortgage plans in Hong Kong.

What is the difference between H-rate and P-rate mortgages?

H-rate mortgages are usually more sensitive to market rate changes, while P-rate mortgages are generally more stable. In low-interest markets, H-rate plans are often cheaper.

What is mortgage insurance?

Mortgage insurance allows buyers to borrow above the standard loan-to-value limit, making it easier to buy a home with a smaller down payment.

Can self-employed borrowers apply for a mortgage in Hong Kong?

Yes, self-employed borrowers can apply, but approval usually depends on income proof and lender assessment. In many cases, the maximum borrowing ratio may be lower than that for salaried borrowers.

What is a refinance mortgage?

A refinance mortgage means moving your existing loan to another lender, often to secure a better rate or more favorable terms.

;){kind=link}

;){kind=link}